- Our Plans

Online PlansNewly Launched

Online PlansNewly Launchedterm-insuranceonline

Super Protect Plus Plan

- It is designed for families with fluctuating incomes

- It comes with a 12-month Cover Continuance Benefit.

- For long-term policyholders, the Special Exit Value returns 100% of premiums paid.

Term Insurance PlansNewly Launched

Term Insurance PlansNewly Launchedterm-insuranceonline

Super Protect Plus Plan

- It is designed for families with fluctuating incomes

- It comes with a 12-month Cover Continuance Benefit.

- For long-term policyholders, the Special Exit Value returns 100% of premiums paid.

Saving Insurance Plans

Saving Insurance Plans ULIP Insurance PlansNewly Launched

ULIP Insurance PlansNewly Launchedulip

ProGrow Plan

- Option to choose a Life Cover Multiple that aligns with your protection needs

- 11 fund options with unlimited switches

- Enhance protection with Rider options

Child Insurance Plans

Child Insurance Plans Health Insurance Plans

Health Insurance Plans Retirement Plan

Retirement Plan Group Insurance Plans

Group Insurance Plans Individual RiderNewly Launched

Individual RiderNewly Launchedrider

Linked Critical Shield Rider

Your Dreams!

Our Linked Critical Shield Rider- Guaranteed Annuity Payout

- Annuity Payout as convenient

- Covers up to 50 critical illnesses

Group Rider

Group Rider

- Our Services

- Claims

- Financial Calculators

- NRI Plans

ULIP Plan

A Unit-linked Insurance Plan or ULIP offers the dual advantage of being an insurance as well as an i... Read More

ULIP Plan

A Unit-linked Insurance Plan or ULIP offers the dual advantage of being an insurance as well as an investment product via market-linked funds. So the premiums you pay not only cover you but also get invested in funds of your choosing.

What Is ULIP (Unit-Linked Insurance Plan)?

How does a ULIP scheme work?

Premium Contribution

You need to pay the premium towards the ULIP insurance plan which you have decided to buy

Life Cover Protection

A certain portion of your ULIP insurance premium is routed towards securing your family’s future and building a financial safety net for your loved ones by way of a built-in life insurance policy. The payout benefit from this is paid to the nominees of the deceased policyholder in case something unfortunate happens to you during the policy term

Wealth Creation Investment

The other part i.e. remaining portion of this premium is then invested in the funds of your choice (equity, debt or even a mix of both)

Which means, not only is your family financially covered in case of any untoward happening (like the life assured’s death), but also your money continues to grow silently in the background and comes to your rescue during the different stages of your life for several important milestones.

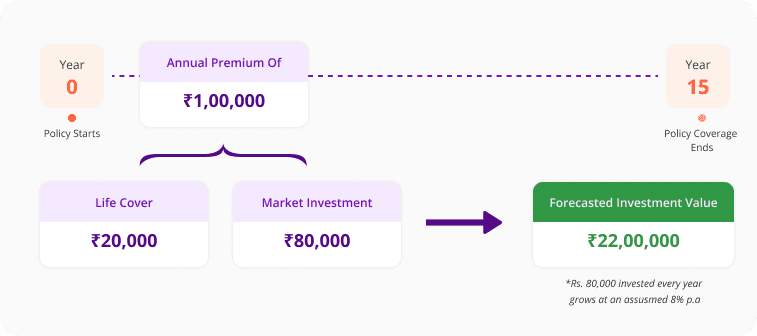

Suppose you pay a premium of Rs. 1,00,000 annually towards your ULIP investment plan for a policy term of 15 years. Out of which, let’s assume Rs. 20,000 may be utilized towards your life cover.

Rs. 80,000 can then be invested in equity and / or debt funds of your choice. Considering an average of 8% growth per year, your Rs. 80,000 investment money can actually grow and become approximately Rs. 22 lakh* over the policy duration of 15 years.

*These figures are for illustration purposes only. Actual returns may vary depending on market performance and fund selection.

Explore OUR plans

tailored for all

Your future needs.

What do you think makes a ULIP scheme so important and special that you must definitely consider adding it to your financial plan this year?

ULIP plan: Key aspects

Beyond just an insurance product

Multipurpose plan (a unique tool that acts as a security / financial shield against life’s uncertainties, while also helping your money grow steadily, in turn creating lifelong value for your dependents)

More control over your current financial journey, because of the inbuilt dual advantages

Flexibility to invest based on your risk appetite

Money mindfulness for your family’s bigger milestones (like your child’s higher education / marriage, your spouse’s retirement plan, your dream home buying goal etc.)

Disciplined savings habit for structured wealth-building purpose

How Does A ULIP Insurance Plan Work?

Wondering how a ULIP (Unit-Linked Insurance Plan) makes your money work hard for you?

Let’s understand with an example :

Annual Premium for your ULIP Insurance:

Rs. 1,20,000

Monthly premium:

Rs. 10,000

Policy Duration:

15 years

Life Cover (as per plan design):

Rs. 12,00,000Investment Allocation :

per year towards your life insurance policy

remaining towards your chosen market-linked plan

ULIP funds are quite different from your traditional insurance plans. Depending on your risk tolerance, financial needs and fund preferences, you can choose to invest your premium in either equity i.e. shares (for higher potential growth, coupled with higher risk), or debt i.e bonds / securities (for stability, and lesser risk). You can even switch between the two fund options for a balanced combination during the policy term (this is suitable for moderate risk takers).

Moreover, ULIP plans offer tax benefits too - by way of deductions under Sec 80C for the ULIP insurance premiums paid. You don’t have to pay any tax on ULIP maturity as well [covered under Sec 10(10D)], subject to prevailing tax laws.

What are the possible outcomes in such a scenario?

*These are indicative values based on assumed returns. ULIP fund performance depends on market conditions, chosen fund mix, and applicable charges.

Key features of a ULIP plan

So, what does your ULIP scheme actually cover? Here are the top 5 noteworthy features in your ULIP insurance plan!

It all begins with the right allocation of your premium to the different purposes that are mapped to your ULIP scheme. The ULIP (Unit-Linked Insurance Plan) premium gets divided into 2 parts fundamentally. Before its allocation, a part of your premium is firstly utilized for ULIP insurance charges like policy administration, fund management etc. Then, a portion of this premium goes towards your life cover contribution.

So, while you build a financial corpus for your family’s future by investing in the right funds, your loved ones can still stay protected throughout. In case something miserable happens to you during the policy term, they shall receive the lump sum payout. Finally, the other part of the premium (balance) is marked as the investment portion, which is routed into funds of your preference.

Benefits of Choosing ULIP Scheme

A step-by-step guide on how the Ageas Federal term life insurance works.

- Higher returns with market-linked growth

- Long-term savings habit

- Option to choose between equity, debt or a balance of both

- Flexibility to switch between different funds during policy term

- Compounding advantage over time

- Tax deduction for premiums under Sec 80C

- Maturity benefits tax-free under Sec 10(10D)

- Disciplined lock-in period built-in

- Goal-based financial planning (kid’s education / marriage, dream house, retirement etc.)

- Two-in-one plan: Life cover + Investment plan

- The financial future of family members secured no matter what

- Systematic contributions (premiums) to build financial corpus

- Optional add-on riders available to enhance protection (like critical illness cover)

- Death benefit is the higher of the two i.e. sum assured or fund value

- Professional fund management with structured investment solutions

- More transparency and better control over your investment as fund value is linked to the NAV (Net Asset Value)

- Easy fund tracking with a hassle-free process - be it at the time of buying the ULIP online or managing it regularly or claiming benefits thereafter post lock-in)

- Single plan, multiple purposes: Growth, savings, financial stability, and protection

- Choose your preferred premium payment mode: Yearly, half-yearly, quarterly and monthly

- Partial withdrawals allowed after completion of lock-in period

Types Of ULIP Plans

ULIPs are thoughtfully designed for versatility, flexibility and specific financial goals. Since ULIP plans come in several formats to suit your varied requirements, financial responsibilities and life goals, they can be categorized on the basis of death benefits, risk appetite, purpose, premium payment options, life cover options, fund options and investment goals. Let’s understand each type of ULIP investment plan in detail. You can pick from any of the following ULIP (Unit-Linked Insurance Plan) options and align the chosen plan accordingly with your financial journey to attain your long-term objectives. ULIP schemes therefore give you the complete control to customize the plan and combine benefits that solely focus on your unique needs, be it wealth creation, protection for family, financial security, peace of mind or a combination of these advantages tailored as per your convenience.

These ULIP schemes are customized based on major milestones such as your retirement, your child’s academic goals or long-term financial corpus creation. Pick a plan that adapts according to your chosen life goal.

-

Wealth Creation ULIPs

Ideally recommended for long-term goals like buying your dream house or saving up for retirement by investing in equity or balanced funds. Example: Your investment of Rs. 1 lakh annually in equity funds for 15 years can potentially grow to become Rs. 30 lakh+ depending on market performance.

-

Child ULIPs

Designed to protect your kid’s academic aspirations and career goals. As it comes with a waiver of premium benefit, even upon the insured parent’s death, the plan stays active and valid in order to secure the child’s future no matter what. Example: Suppose you decide to pay Rs. 50,000 annually as premium towards the ULIP scheme for the next 15 years. If something unfortunate happens to you in the 7th year, the insurance company shall continue to pay the premium on your behalf, keeping the policy unaffected till maturity, in turn, safeguarding the corpus for the child.

-

Retirement ULIPs

As the name suggests, this is best suited for your retirement plans. As you near your retirement age, the plan makes room for stability by giving you the opportunity to even switch to debt funds from equity funds. You can also opt for regular pension payouts in certain plans.

How To Invest In A ULIP Plan For Long-Term Benefits?

Investing in a well-thought-out ULIP (Unit-Linked Insurance Plan) can be extremely rewarding. Think of it like your long-term financial planning partner; someone you can rely on to protect your dear ones when you are no more around to fulfill their financial requirements, a trusted companion to look after your investment and ensure that it appreciates with time, to provide you with the desired safety net at maturity, in order to achieve several key milestones without exhausting your savings or depending on any loans. And lastly, it’s a smart financial tool that maximizes your savings potential.

How you can make sure your ULIP scheme delivers long-term benefits: A detailed guide

What is it that you are investing in the ULIP scheme for? Is it to cover your child’s marriage expenses, support your dream of buying your own house, or are you saving up for your spouse’s retirement needs?

Based on your chosen objective, you can accordingly determine -

- your policy term (i.e. for how long do you want to stay invested in the plan?) and,

- your risk appetite (which of these funds, whether equity and / or debt, do you want your contributions to be invested in?) etc.

How To Buy A ULIP Plan Online Through Ageas Federal?

Explore ULIP Plans

Compare & Understand

Check Eligibility

Choose the Right Plan

Calculate Your Returns

Customize Your Plan

Complete KYC & Risk Assessment

Make Payment

Policy Issuance & Welcome Kit

Why should you buy ULIP funds online?

Hassle-free application process

Hassle-free application process- Comparing, assessment and purchase of the plan: All can be done right from the comfort of your house

- Use of free online ULIP calculator for easy calculations

- Zero paperwork, exclusive online benefits

- Immediate access to your portfolio promoting transparency and trackability

Who Should Invest In A ULIP Scheme?

Facts You Should Know Before Investing In A ULIP Insurance Plan

Twin benefit

Financial safety net for long-term needs + Life cover protection in case of policyholder’s death

Death benefit

Higher of sum assured or fund value

Choice of the premium payment

Pick according to your cash flow needs

Flexibility to switch depending on market volatility

Change between equity, debt and balanced funds during the policy term

Lock-in period

Generally speaking, a 5-year lock-in period is mandatory. This encourages staying invested for a longer duration of time

Power of compounding

Your contribution → Returns on this contribution based on your risk preference → Compounding effect → Consistent savings over time → Higher payout lump sum at maturity → Life goals safeguarded from future financial uncertainties

Market-linked plan

You have complete control over your investment - whether you want to opt for equity (stocks), debt (government bonds and securities) or a mix of the two (balanced funds) - based on your risk attitude and fund performance

Tax benefits

Deductions for premiums + exemption at maturity + tax-free switches between funds during policy term

Partial withdrawals allowed

Got urgent needs? Withdraw freely during emergency situations once the lock-in is over

Policy charges

ULIP schemes do come with specific upfront charges which are regulated (such as mortality charges, fund management, premium allocation etc.)

What Is A Unit-Linked Insurance Plan Calculator?

Assess how your investment is expected to grow over the policy duration

Know the indicative lump sum payout beforehand to align the maturity value with your life goals

Decide your investment contribution (premiums) based on easy calculations provided by the tool

Strategize between different fund options to maximize your advantage

Get a real perspective, or a much-needed reality check regarding what kind of wealth accumulation benefits can be received from your ULIP investment plan

AGEAS FEDERAL LIFE INSURANCE

Endorsed by Life Insurance Experts

Ageas Federal Is A Trusted Life Insurance Partner

At Ageas Federal Life Insurance, we are dedicated to creating meaningful insurance solutions that help individuals build a secure and confident future. With over a decade of experience, we offer a wide range of plans across protection, pension, savings, investment, annuity, and health, designed to support evolving financial needs at every stage of life.

FAQ’S related to ULIP Plans

Before choosing to invest in a ULIP, you should know these 3 things: • There are some fees and charges • Know the funds that suit your investment strategy • ULIPs are beneficial in the long run. So you should have the discipline to stay invested throughout the policy tenure

You can always choose to invest more or your entire amount in debt funds to minimise the risk. Moreover, you can alter your investment strategy depending on the market scenario by switching between equity and debt funds.

The major apprehension most policyholders have is - ‘What is my tax liability on ULIP maturity?’ Well, the best part about ULIP funds is that you can enjoy dual advantages - disciplined savings for the long term, and tax savings for the financial year (subject to prevailing tax laws). This makes a ULIP plan the best investment decision that you can ever make for your own future financial security along with risk protection for your family (upon the insured person’s untimely death). Let’s break it down further -

- Tax deductions on premiums paid towards your ULIP scheme [under Sec 80C] For example, your annual premium is Rs. 1,20,000, you can claim the entire amount as a deduction, thereby reducing your taxable income (maximum limit = Rs. 1,50,000 deduction allowed under this section).

- Tax-free maturity value [under Sec 10(10D)] For example, you invest Rs. 1,00,000 every year in a ULIP scheme for 10 years. Total Investment = Rs. 10,00,000. Let’s assume your fund grows to Rs. 16,00,000 at maturity. Under this section, Rs. 16,00,000 is completely tax-free (subject to certain premium conditions).

- Switches between fund options are also tax-free.

Thus, ULIP funds are smart investment plans with double-savings-benefit rolled into just one single product (i.e. savings enabled for not just your future but also your present financial position), ensuring complete tax efficiency in the hands of the policyholder.

In return for the premium amount you pay (i.e. the portion of premium invested after deducting the life cover component and the policy charges as applicable) towards the equity, debt or balanced funds of your choice, you are offered “units” based on the prevailing Net Asset Value (NAV) of that fund. For example, suppose Rs. 1,00,000 is your annual premium. After charges, Rs. 95,000 is invested. If NAV of the chosen fund is Rs. 25, then here’s how you can calculate the units allotted. Number of units allotted under ULIP scheme: 95,000 ÷ 25 = 3,800 units. Based on the market performance, the NAV increases or decreases. Accordingly, your ULIP fund value also fluctuates. When you buy a ULIP plan online on Ageas Federal, you can easily track your investment, its NAV and regularly review your fund’s performance.

The full form of NAV is Net Asset Value. NAV is the price of each unit in the ULIP fund that you hold on any particular given day. Just like mutual funds, NAV represents the market value of the fund’s investments after deducting charges. Which means that when you invest, your money is used to buy units based on the NAV on that day. Over time, as the fund grows, the NAV also rises, in turn increasing your investment value.

Formula: NAV = (Market Value of Fund Assets – Charges) ÷ Number of Units Outstanding

Illustration: Let’s say your fund has assets worth Rs. 100 crore. After deducting charges, suppose the net value comes to around Rs. 99 crore. Now let’s assume that there are 10 crore units issued. The NAV is then calculated at Rs. 9.90 per unit.

FOLLOW US ON

Copyright © 2026 Ageas Federal Life Insurance Co Ltd. All Rights Reserved.