When you can’t be there anymore, your term life insurance plan stays, committed to its goal of ensur... Read More

Term Insurance

When you can’t be there anymore, your term life insurance plan stays, committed to its goal of ensuring that - your family is well taken care of financially, protecting their confidence, dreams and future, with ONE MOST POWERFUL PLAN that works harder, to unlock a large sum which can, in your absence, act as - an income replacement for their day-to-day expenses, a safety net for your child’s higher education / wedding cost, and a financial cushion to pay off any loans, and maintain their lifestyle.

What is Term Insurance?

A term life policy is nothing but simply a form of life insurance cover, to offer financial

protection to your family, by way of a small sum paid regularly as premium over a fixed period

i.e. the “term”. Upon death of the insured person during the policy term, the nominee shall

receive the sum assured as per the terms of the policy. If the insured person survives this term,

then there is generally no payout, unless the insured person has opted for a term life insurance

plan with a built-in ROP (Return Of Premium) feature. The Ageas Federal term life insurance plan

is a promise of security for your family’s priceless future, when you are unfortunately not around

anymore to guard it. And do you know what’s best about these term life insurance plans?

Affordable premiums that guarantee complete peace of mind - for as low as the cost of your

monthly OTT subscriptions (or a few coffees maybe!) - ensuring a huge safety net worth lakhs

to crores of coverage for your loved ones, especially during the most testing times. A best term

insurance plan can keep your family’s dreams alive when you cannot. A simple yet smart way to

make certain that, in future your loved ones don’t feel the financial gap caused by your sudden

death, is to buy term insurance today. When life takes an unexpected turn, even in your absence,

you can establish lifelong security for your beloved ones with the Ageas Federal term life policy.

In other words, your care takes the form of a crore-worth cover at the right time, offering pure

protection and certainty to your family in life’s unstable moments.

Read More...

Explore OUR plans

tailored for all Your future needs.

How Does A Term Insurance Policy Work?

A step-by-step guide on how the Ageas Federal term life insurance works.

Cover amount is the guaranteed amount of money, received as payout upon death of the life assured during the policy term, which acts like a financial umbrella over the nominees of the policy

The Checklist - Things To Keep In Mind

Choose a cover amount i.e. sum assured depending on the following factors

Big milestones in future (child’s education and marriage, retirement coverage for spouse etc.)

Everyday expenses for next 10-15 years

Any pre-existing loans and ongoing EMIs (car loan, home loan, personal loan…)

The Cover - Sample Scenario

If you are earning 10-15 LPA, it is recommended that you consider a Rs. 1-3 crore term life insurance cover

The Concept - What It Is

Policy term is the chosen duration for which you would like protection from the term life policy. That is the number of years during which your family can stay secured under the plan

The Checklist - Things To Keep In Mind

The longer the policy term, the more years your loved ones stay covered (which also means, the longer the policy term, the higher your premium usually is, because covering you for more years means more risk for the insurer. For instance, a Rs. 1 crore term insurance cover for 15 years period may cost Rs. 500 premium per month, for 25 years - Rs. 700 per month, and till age 80, Rs. 1200 per month)

You can choose either of the following terms:

A specific number of years (say 25, 30, 35, or 40 years)

Till you turn a certain age (say 60, 70 or even 80 years)

You can go for short term (10-15 years), medium term (20-30 years), and even long term (40+ years till age 99) depending on your age, risk profile, financial goals, expected level of family support in future etc. The term life insurance may accordingly end sooner, or stay for a balanced duration extending through your prime earning years to fulfil a long promise of protection

The Cover - Sample Scenario

If you opt for a 40-year policy term at your 20 years of age, your family is protected under the term life insurance cover till your age 60 and shall receive the sum assured if anything unfortunate happens to you during the policy term

The Concept - What It Is

There is complete flexibility to select when and how you want to pay towards the term life insurance premium

The Checklist - Things To Keep In Mind

There are several premium payment options that you can choose from -

Regular pay (Monthly, quarterly, half-yearly and annual premium

Limited pay (End premiums early in a few years)

Single pay (One-shot premium)

Regular pay is best for individuals who prefer smaller payments consistently because it is easily manageable for them

Limited pay is perfect for those who want to finish paying premiums beforehand. There is no obligation to pay anything later after the completion of the predetermined initial few years. Also, these policyholders may not really mind the slightly higher cost involved, as the family security applies till the end of the policy term

Single pay is ideal for people who like to get done with the payment of premium right at the start of the policy term by investing the lump sum funds that they have. They can handle the highest upfront cost inbuilt in this option since they value the maximum convenience it brings along with one-shot payment style

The Cover - Sample Scenario

One-time, a few years, or every year – your choice

Payment flexible, protection fixed

If you decide to go for a policy term of 25 years, but want limited pay premium option (for 10 years) enabled in your term insurance, then you shall pay premium for just first 10 years, with protection that extends over the entire policy term of 25 years

The Concept - What It Is

You are required to provide information about your health and lifestyle habits transparently, undergo and submit medical test reports as mentioned in the form, upload necessary documents for KYC and financials whenever you buy term insurance online

The Checklist - Things To Keep In Mind

You need to answer some simple questions to complete the formalities when you buy a term insurance policy. These declarations about your health and lifestyle and in some cases, even your medical tests are extremely important for the insurer to arrive at a conclusion regarding your risk profile, and accordingly decide your premium amount. After which, certain standard documents like Aadhaar, PAN, income proof, and address proof, are also required to fulfil eligibility criteria and a hassle-free KYC process

The Cover - Sample Scenario

Subiksha, 34, needs to buy a Rs. 1 crore term life insurance online for herself. She has all her documents in place - Aadhar, PAN, 6-month salary slips, and address proof. She has submitted these in order to buy term insurance online on Ageas Federal Life Insurance website. Her documents are thoroughly vetted and post verification, her term insurance gets issued in the next 48-72 hours without any hassles

Rishabh, a non-smoker, 29, is planning to buy a term plan online. No medical history found. He needs to pay a basic premium as calculated for his profile

In scenario 2: Rishabh smokes regularly and has diabetes. He needs to pay a slightly higher premium compared to scenario 1 above. The insurer can even ask for a medical report before initiating approval of the policy

The Concept - What It Is

Underwriting is a crucial process - basically consisting of background checks before the policy takes off - to review your health, lifestyle, medical and financial report card and decide the premium before approving your application

Think of underwriting like a referee’s whistle before the game or the security check at the airport

The Checklist - Things To Keep In Mind

Much like the concept of product-market fit, underwriting helps find if the chosen policy matches with the individual’s profile (It’s a mandatory check done to arrive at the perfect policy-insured person fit). It’s like a gate pass or green signal to match and align the right coverage with the financial needs of the applicant

Post this procedure, your policy is issued and your family stays secured from this moment till end of the policy term, as the term life insurance protection is officially considered active from hereon

A soft copy of the policy document is sent immediately to your email and a hard copy is then couriered to your address as proof

The Cover - Sample Scenario

Ranveer, 37, has submitted an application online for a Rs. 45 lakh Ageas Federal term insurance cover. After clearance regarding his health data, medical reports, and financial statements, the policy is issued and his family is covered from the date of issuance

The Concept - What It Is

There are two situations to primarily consider for this:

Death of the life assured during the policy term

Survival of the life assured till end of the policy term

The Checklist - Things To Keep In Mind

In situation one:

In an unfortunate event of the insured person’s death during the policy term, the nominee shall receive the sum assured as per the payout terms mentioned in the policy document

In situation two:

If the insured person survives the policy term, depending on ROP (Return Of Premium) opted (this feature is available in certain term insurance policies), the insured person - at the time of maturity - shall receive the total base premiums paid

The Cover - Sample Scenario

Shilpa, 32, holds the best term insurance for Rs. 1 crore for a policy duration of 30 years.

In scenario 1:

If Shilpa passes away during the policy term, her husband (nominee) shall get the sum assured i.e. Rs. 1 crore either as lump sum payout or monthly income or a combination depending on the payout option chosen by Shilpa before policy issuance

In scenario 2:

If Shilpa outlives the policy term and has chosen term life insurance with ROP (Return Of Premium, she shall receive all base premiums paid over the last 30 years

Who Should Buy A Term Plan?

The best part about a term insurance policy is that it doesn’t differentiate between different categories of people. It works for everyone who has someone dependent on them financially.

Plan? Just ONE! Who does it benefit? Many like YOU!

Let’s begin with the example of the primary earners i.e. breadwinners of the household, the main group of individuals who must definitely buy a term insurance policy. Why? When you are the sole financial contributor in the family - be it an employee or an entrepreneur, your sudden absence stops the financial engine immediately.

To keep things running like before i.e. to pay bills, support lifestyle of dependent members upon the insured person’s death, and to provide urgent and regular financial assistance to the family members for their different needs arising from time to time, a term life policy is the most ideal recommendation by several finance experts, so that your main source of income can be replaced effectively with one smart insurance decision.

Young parents and couples who are planning for a family can also consider buying a term plan, as starting early when it comes to term insurance gives you the ‘less premium, higher sum assured’ advantage. You can thus plan for your child’s future right from today - be it for their education, marriage or other bigger dreams, and pass on your token of love with the help of the Ageas Federal term life insurance plan.

Loans and EMIs are long-term commitments and even in your absence tomorrow, they won’t automatically disappear. They can cause extreme financial stress to your family members. If you are someone with big commitments or in case you have availed home loans with repayments scheduled for the next 15-20 years, with a best term insurance policy, you can ensure a wealth shield cum security blanket for your loved ones so that they don’t have to risk losing the house or liquidating assets to pay off your huge debts.

Sometimes, it is not just about your family, but also about the key partners who are financially impacted when something drastic happens to you. Hence, if you are a business owner or a key stakeholder elsewhere, the term life insurance in such cases, becomes an invisible helping hand offering the much-needed stability to your other ventures. There is no need for your dependents then, to compromise on their personal finance to ensure business continuity.

Usually, the dependent members are (but are not limited to) your spouse, parents, children, siblings, and extended family members who feel the immediate financial strain upon the death of the insured person. Therefore, a term life insurance plan is designed in such a way that it brings the family’s financial journeys back on track. When life snatches the care and physical presence of a beloved person, their commitment towards their family still continues, and thrives to fill the void in the form of a term insurance cover.

Why Buy A Term Insurance Policy?

Here are thirteen compelling and undeniable reasons why you must immediately consider buying a term insurance policy. The benefits of term insurance extend beyond just protection, and that’s precisely why every family needs a term life insurance to protect their tomorrow from life’s harsh uncertainties.

The best term insurance plan, that’s ideally suited for your family’s specific future financial needs, acts as an income replacement option for your loved ones, to fund their everyday expenses and lifestyle maintenance, especially because you may no longer be there to provide for them.

What Are The Benefits Of Buying A Term Insurance Plan?

There are several advantages of term life insurance which make it a winning insurance product even today and an evergreen financial instrument yielding stability for your family:

Straightforward policy for future financial protection

Affordable premiums (cost-effective plans with attractively higher coverage)

Convenient payout options

Simple claim process

Option to choose term life insurance with Return Of Premium (ROP)

Family’s day-to-day financial needs taken care of after your untimely death

Policy accessibility for different groups of people (young earners, women, near-retirement individuals, people with huge debt burden, people with low risk appetite etc.)

Several types of term insurance plans to pick and choose from depending on your specific financial situation

Easy policy terms (i.e. the flexibility to align policy duration and premium paying term according to the budget that you can allocate)

Term insurance specific tax benefits (deductions for premiums paid, and completely tax-free death benefits)

Customizable term life insurance with add-on riders available for additional coverage and complete protection

Hassle-free and quick settlement record

Financial burden waiver for the family as it acts like a safety net for loan repayment

Life quality of dependents secured

Life stage benefit and increase sum assured feature

Protection partner for your hard-earned assets so that they can remain with your family

Common Features Of Term Life Insurance

Term life insurance plans are basically financial protection instruments designed for your family’s security, future financial stability and the policyholder’s peace of mind. The most common features of a term life policy are:

How To Pick The Best Term Insurance Policy In India?

If you are thinking of purchasing a term life insurance plan anytime soon, ‘someday’ is not really the perfect time, instead ‘today’ is the right time. However, how can you make sure that you pick a term insurance cover that’s most ideal for you, your family goals and financial commitments? All you need is a checklist with top factors you must consider before buying a term insurance policy in India. Remember that it is never about picking the cheapest option from the policies. Here’s what you must bear in mind:

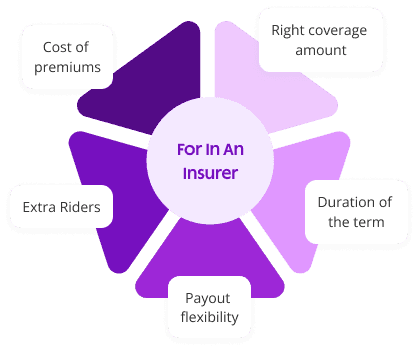

Factors To Look For In A Term Life Policy

Your sum assured has to be adequate enough to fulfill outstanding loan obligations, fund important life events like kids’ education, parents’ medical needs, spouse’s retirement goals etc., and also replace your income effectively. Choose a term life policy that can secure your family’s future financial journey. Likewise, the policy term should ideally cover your working years, spanning either till your retirement or till your major financial responsibilities are completed.

Those are exactly the years when your loved ones are financially dependent on you and your untimely death can make them not just emotionally vulnerable but also financially weak. In some cases, it’s best to get the entire death benefit as a lump sum amount, whereas in certain situations, a monthly income option may work suitably well for your family’s needs at that point in time. Hence, always check for payout flexibility before deciding which term insurance to buy. Extra riders added to your term life insurance, provide additional protection over and above the sum assured for very specific cases like accidental death, critical illness etc., at a very nominal cost. In essence, make sure that the amount of premium is affordable throughout and adjusted according to your short-term and long-term goals, desired coverage amount, policy duration and premium paying terms, so that you can stay invested for a longer period of time and your family isn’t exposed to any life-altering event prematurely.

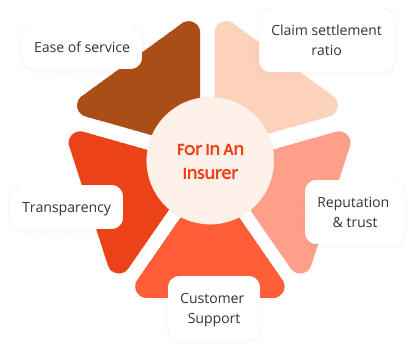

Factors To Look For In An Insurer

Let’s start by understanding what claim settlement ratio looks like for the best term insurance companies. A higher claim settlement ratio in term insurance indicates the insurer’s commitment to honoring claims, putting you and your family at ease, before trusting them with such an important financial decision of your life. You need to also verify and conduct background checks about the insurer.

Ensure you do a thorough investigation of the insurance company’s financials, their track record, market standing, economic performance, overall credibility in the industry, presence across the country, positive customer responses (reviews / ratings / feedback / testimonials) and past claim settlement records before buying your term life insurance policy from them. What is the digital ease of buying your term plan looking like on their platform? What kind of assistance does their customer support team offer?

For example: Term insurance guides for easy understanding, jargon-free communication and language throughout so that you exactly know what you are signing up for, real-time / all-day chat / calling support, insurance advisors along the way, quick policy issuance, same-day dedicated claim processing, responsive service, discounts for purchasing online, add-on benefits, so on and so forth. How transparent does the process of buying, managing the policy, paying the premiums, and claiming benefits look to you? Based on your evaluation and assessment of the above parameters, make an informed decision when it comes to choosing the best insurance company for your term cover.

When Should You Buy A Term Insurance Plan?

The answer is ‘today’. That’s how soon you should be considering buying a term life insurance plan because the advantages of starting young in a term life policy are just so unmissable. The earlier you begin, the more benefits you get - tailored low-cost plan, affordable premiums, long-term protection, extended coverage, peace of mind for a longer period of time, financial security for big and important events (like marriage, home buying etc.) and so on. Throughout your prime working years, you can be stress-free that your family’s needs shall be taken care of if something bad happens to you. Your age and health are two main components considered while deciding your term insurance premium. So starting soon when you are in the pink of health makes your premium cost-effective in the long run.

Age 25-30

Starting Early

Lowest premiums when you’re young & healthy

Lock in low costs for the long term

High coverage at minimal expense

Stress-free protection from day one

Age 30-45

Life Takes Shape

Protect your spouse’s long-term financial future

Secure home loans and ongoing liabilities

Increase coverage as responsibilities grow

Age 45-60

Stability & Security

Strong financial safety net during vulnerable years

Protect dependents as income responsibilities peak

Insurance steps in right when it’s needed most

For each phase in your life, you can enjoy attractive and comprehensive coverage, while also paying less compared to someone who starts late. That is, if you want to take a home loan, in case you have dependent parents, if you are planning to get married and want to ensure your spouse’s long-term financial protection, or in case you are a young parent expecting a big expenditure in future for your child’s education / marriage, then a term life insurance policy purchased in your 20s / 30s provides the benefit of a huge sum assured (coverage amount) that can manage all these obligations, essentially without any restrictions. Moreover, starting at a young age helps you lock in a relatively low premium for a longer duration of time i.e. up to 40 years (policy term) and even more.

When you are more vulnerable financially, and when your family is directly dependent on your income for their basic needs and also their future dreams, your term insurance cover takes your place with immediate effect (i.e. when you need it the most, when you are no more). Even if you are slightly older or are already in your near-retirement phase, a term life insurance plan is still the best option for your family’s goals at different stages of life. With term insurance, your family can minus the stress of managing it all by themselves without you around. Because, the payout from your term life insurance will be just around without any delay to help them on your behalf.

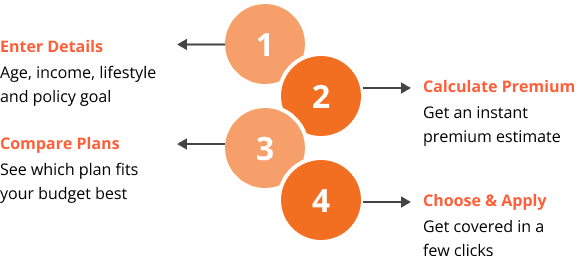

How To Calculate Term Insurance Premium Online?

You can use the online calculator option available on Ageas Federal Life Insurance website to estimate your term insurance premium amount. This way, you can make an informed decision, after fully understanding what you need to pay, if you opt for only a basic term life policy versus what amount you should be paying additionally if you want to combine any of the riders with your base plan.

After entering your basic information like age, desired sum assured, income level, gender, lifestyle habits, health data, and the policy term that you are looking at, the online term insurance calculator, with the help of actuarial frameworks, estimates the amount you need to be paying. This makes your life very easy, giving you an upfront calculation, in order to arrive at a conclusion regarding your term insurance. Using the online calculator, you can even compare several term insurance plans in one go and pick the best term insurance that’s tailored for your budget.

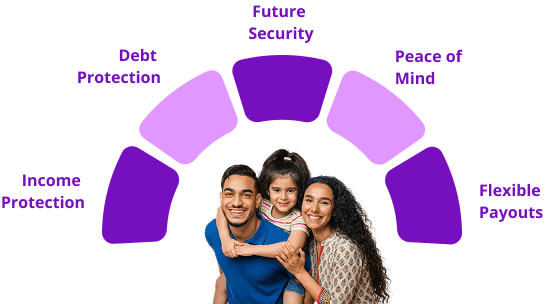

How To Secure Your Family’s Future With A Term Life Insurance Plan?

Beyond its advantages as an excellent insurance product, a term life policy surprises you in more ways than one, when it comes to being there for your family when you can’t be. Here’s how the best term insurance secures your family’s future.

What if the family needs the death benefit altogether as a lump sum? What if your spouse prefers monthly income from the payout money? Both these can be managed. Even a combination of the two methods is possible. You can choose your preferred payout option at the time of purchase of the term insurance plan.

As life progresses, risks multiply. Add-on riders provide better coverage for specific cases like accidental death, critical illness etc. beyond the coverage amount determined in your basic term life insurance plan.

A good term insurance acts like an income replacement when your family needs it after your death to fund their day-to-day expenses and lifestyle.

Term life insurance payouts can be utilized to repay your home loan, personal loan, education loan etc. Liabilities need not be inherited anymore!

What about a financial safety net for your family’s future goals like kids’ higher studies and wedding expenses, spouse’s retirement plans and your parents’ medical needs in old age? Worry no more! Even in such situations, your term life policy actually comes to your rescue

Knowing that your family won’t be dependent on anyone in future after you are gone, gives you the much-needed confidence today to plan better and invest in various other financial instruments, both for your own personal development and your family’s welfare.

What if the family needs the death benefit altogether as a lump sum? What if your spouse prefers monthly income from the payout money? Both these can be managed. Even a combination of the two methods is possible. You can choose your preferred payout option at the time of purchase of the term insurance plan.

As life progresses, risks multiply. Add-on riders provide better coverage for specific cases like accidental death, critical illness etc. beyond the coverage amount determined in your basic term life insurance plan.

A good term insurance acts like an income replacement when your family needs it after your death to fund their day-to-day expenses and lifestyle.

Term life insurance payouts can be utilized to repay your home loan, personal loan, education loan etc. Liabilities need not be inherited anymore!

What Are The Payout Options Available In Term Life Insurance?

Your term insurance policy recognizes that a one-size-fits-all approach may not be ideal and beneficial, especially during claim payouts. Hence, irrespective of when the death benefit shall become payable to the nominees of the policy, the term life insurance cover offers this option - to determine the payout mode - directly to the policyholder, right at the start before they buy the term plan. The policyholder can thus choose a method that aligns with their family’s financial responsibilities. Which means you get to pick one of the following payout options that’s most convenient and suited for your family’s evolving needs.

Here’s how customizing payouts works in your favour:

Lump sum payout

Under this option, the full sum assured is paid upfront, in one go. This works best for families that need a lump sum amount for their immediate liabilities such as loan repayment, bigger expenses like that of their child’s marriage etc.

Monthly / Regular Income payout

As the name suggests, under this, you can choose to enable smaller payments but regular income for your nominees instead of one single payment as a whole. This helps in ensuring a fixed source of earnings for the loved ones of the deceased, acting as an income replacement option for them. Unlike lump sum payout, wherein a safety corpus can be created, in regular income payout, stable financial support for a certain period of time is prioritized over wealth creation, covering the everyday expenses and short-term goals of the family members.

Combination of lump sum + income payout

This integrates the benefits of both the payout options. Here, a portion of the sum assured is paid as a lump sum amount. The remaining part is paid as regular payouts during a chosen period, thus helping achieve the family’s immediate and long-term financial goals.

How To Apply For A Claim In Term Life Insurance?

The term insurance claim process is usually kept extremely simple, so that the family members of the deceased policyholder, who may be already grieving the loss of their loved one, can apply without any hassle or complications to avail the death benefit due to them.

Here’s what you need to keep in mind in case you are the nominee. The following steps are to be followed to claim the coverage amount if the policyholder passes away during the policy term.

Intimate the Insurance Company

Fill the claim form

Submit essential documents

Claim review and verification

Claim settlement

Claim rejection

Firstly, make it known to the insurer, that the individual who was holding the term life policy in their company has passed away, through the customer care executives online or at the branch directly.

Intimate the Insurance Company

Firstly, make it known to the insurer, that the individual who was holding the term life policy in their company has passed away, through the customer care executives online or at the branch directly.

Fill the claim form

Submit essential documents

Claim review and verification

Claim settlement

Claim rejection

Steps To Buy A Term Insurance Plan Online

Buying a term insurance plan online is very easy. There are just seven simple steps to be followed when you apply for term insurance. The entire process can be completed online without any hassles. Here’s how it works -

STEP 7 :

Paying premium and activating your term life insurance plan

Once the premium is paid, and the verification is done, your policy is then approved after underwriting formalities are over. The coverage is officially considered active from here onwards and your family stays protected till the end of the policy term provided all premiums are duly paid.

STEP 1 :

Understanding the agreement

The process begins with a contract / agreement between the insurer and the applicant which states that - in return for the premiums that you agree to pay over a specific duration (policy term), the predetermined sum assured shall become payable to the nominee, upon the death of the policyholder during the policy term. That is, the insurer promises financial protection to the family members if something untoward happens to the insured person within the term. This is the first step you need to take in order to understand how the process of buying the term plan and managing it works from here onwards.

STEP 2 :

Assessing your needs

This is done to determine the exact coverage amount with clarity. Calculations are made based on what your family situation looks like - their financial needs, goals, and habits and what your commitments are towards them, in the sense, your loans, your current financial status, standard of living, your future dreams for family, obligations that may arise in the short-term and the long-term and most importantly, your age, health and income level.

STEP 3 :

Choosing policy duration

Your policy term must take into consideration your age, desired sum assured, premiums you can afford based on availability of funds, your working years, your family’s dependent years on your earnings, and your retirement age goal.

STEP 4 :

Comparing term insurance plans and premiums before purchase

Analyze several aspects critically before concluding that this policy is the ONE for you. Factors you must consider: Affordable premiums, flexible payouts, long-term protection, higher sum assured, extra benefits and discounts, service delivery and customer support, previous track record of the term life policy insurers that you are considering, their claim settlement ratios, digital ease and convenience, policy features etc.

STEP 5 :

Filling application form

Submit your personal, medical and financial information truthfully. Make all declarations about your health and lifestyle with complete honesty to avoid any issues with your term insurance policy claim later.

STEP 6 :

Getting medical check-up done if required

Submit medical reports wherever required and undergo health tests as directed.

STEP 7 :

Paying premium and activating your term life insurance plan

Once the premium is paid, and the verification is done, your policy is then approved after underwriting formalities are over. The coverage is officially considered active from here onwards and your family stays protected till the end of the policy term provided all premiums are duly paid.

STEP 1 :

Understanding the agreement

The process begins with a contract / agreement between the insurer and the applicant which states that - in return for the premiums that you agree to pay over a specific duration (policy term), the predetermined sum assured shall become payable to the nominee, upon the death of the policyholder during the policy term. That is, the insurer promises financial protection to the family members if something untoward happens to the insured person within the term. This is the first step you need to take in order to understand how the process of buying the term plan and managing it works from here onwards.

Term Insurance : Important Jargons Explained

Premium

The amount that you must pay regularly to the insurer to keep your term insurance coverage on.

Sum Assured

The death benefit / coverage amount / claim payout that the family (nominee) receives upon the death of the policyholder during the policy term

Policy Term

The number of years for which your policy stays active and your family enjoys coverage / protection.

Premium paying term (PPT)

This is not the same as a policy term. PPT is the number of years you want to pay your premiums for. If you have a policy term of 40 years, and a PPT of 20 years, after the first 20 years you don’t need to pay any premiums, yet you can stay protected under the term life insurance plan for the entire duration of 40 years.

Nominee

The individual (appointed by policyholder) who is entitled to receive the sum assured (claim amount) upon the death of the policyholder during the policy term.

Grace Period

The window provided (extra time given after due date) to pay the overdue premiums in order to avoid policy lapse.

Riders

Additional covers enabled optionally alongside your base term life policy for enhanced protection and wider coverage.

Exclusions

Specific situations / causes of death which are not included in your term insurance cover (for instance, suicide in the first year of policy).

Underwriting

The process undertaken to assess your risk profile; also decide your premium and eligibility based on your age, health, coverage you have applied for, income, lifestyle and your financial commitments towards your family's future.

Claim settlement ratio (CSR)

The percentage of claims settled by the insurance company out of the total claims received in a year. The higher the claim settlement ratio, the stronger the insurer’s trustworthiness. Which means that greater are your chances of a hassle-free claim settlement experience with the insurance company. The CSR metric helps you gauge the insurance company’s commitment to honor your claim during critical times.

Return Of Premium (ROP)

A feature / policy variant that you can opt for during the purchase of the term life insurance plan, in case you wish to obtain back all the premiums paid till maturity, if you outlive the policy term.

Revival Period

The window (maximum time limit) provided to reactivate a term life policy that has lapsed due to outstanding premiums.

AGEAS FEDERAL LIFE INSURANCE

Endorsed by Life Insurance Experts

Ageas Federal Is A Trusted Life Insurance Partner

At Ageas Federal Life Insurance, we are dedicated to creating meaningful insurance solutions that help individuals build a secure and confident future. With over a decade of experience, we offer a wide range of plans across protection, pension, savings, investment, annuity, and health, designed to support evolving financial needs at every stage of life.

FAQ’S related to Term Insurance Plans

Term insurance is the most simple and straightforward form of life insurance, which is not only affordable, but also highly preferred and considered essential by insurance experts for its coverage size. In case something happens to you during the policy duration (policy term), the term life insurance plan promises financial security to your loved ones. Since term life policies are primarily designed to act as financial instruments for family protection and not high-risk market-linked investments yielding attractive returns, there is generally no payout at maturity if you survive the term (unless you opted for a term life insurance with ‘Return Of Premium’ plan). The key highlight of any term insurance policy is its ‘low cost of premium for a high coverage amount’ benefit. So, a 25-year-old young professional, with clean health records and a non-smoker status, can buy a Rs. 1 crore term insurance plan at an annual premium of just a few thousands. That is, for as little as Rs. 800 - Rs. 1,000 per month. If you pass away during the term, the lump sum payout from your term insurance cover protects your family members from financial distress, especially because your income and earnings are no longer available to them. Your dear ones can use this death benefit to repay your loans, fund their dreams, afford major milestones like higher education, marriage, etc., invest in other financial instruments for a better future, maintain their standard of living, live with dignity in their old age / retirement period, all this and more while keeping you in their memories for your one wise decision, your sheer commitment to secure their future with the best term policy. Often requiring just basic documents and a few medical tests based on your age and health / lifestyle factors, online term insurance covers are super easy to understand, buy and claim. You can also customize your term insurance coverage for comprehensive protection by adding riders like accidental death benefit, critical illness cover, waiver of premium, and / or disability cover.

So, what do you think makes the term life insurance plan a smart financial choice for policyholders? Well, the answer is simple. Multiple tax benefits!

Section 80C - Premiums paid towards your term insurance plan are eligible for tax deductions (up to Rs. 1.5 lakh annually).

Section 10(10D) - The death benefit / payout (sum assured paid to the nominee) is completely tax-free.

Section 80D - If you have added health-related riders like critical illness or disability cover, premiums for those may also qualify for deductions under this section.

For example, if you pay Rs. 20,000 towards your term life insurance as annual premium, this amount can be claimed as a deduction under Section 80C, which reduces your taxable income. If the unfortunate event of death happens during the policy term, and your nominee receives Rs. 1 crore sum assured, the entire payout is tax-free in their hands

When you buy a term insurance policy, keep these documents handy to ensure that you have a stress-free experience and quick policy issuance as you apply for the coverage you desire. You are expected to provide accurate information in these documents. If any of these documents or details provided in your application are found to be forged and invalid, your claim can get rejected later.

Identity proof (Aadhaar, PAN, passport, voter ID)

Age proof (Birth certificate, Aadhaar, driving license)

Income proof (Salary slips, Form 16, ITR, bank statements [to justify the sum assured you are applying for])

Medical reports (Depending on your age, occupation, health declarations made, and sum assured mentioned in the application, the insurer may want you to undergo medical examination or reports may have to be submitted as required)

Photographs (Passport-sized photos for records)

Yes, you can buy multiple term insurance policies from different insurance companies. This allows you to diversify benefits from several term insurance covers while also scaling protection with increased sum assured from multiple plans. However, make sure to disclose about each of your term life policies to all your insurers because insurance companies generally tend to check the overall eligibility of the policyholder to ensure alignment of your income with your desired total coverage amount.

Multiple term insurance covers means more flexibility for the policyholder because you need not overpay or overcommit at an early age. Instead, your term life insurance covers can be structured based on your financial responsibilities at different life stages. Your nominees can claim payouts from all policies you hold at the time of death, thus leading to lump sum benefits helping in their immediate and long-term financial relief.

Example: Anuradha, a 28-year-old non-smoker, healthy female, buys a Rs. 50 lakh term insurance plan, with the goal of providing financially for elderly care expenses of her parents, upon the likelihood of her untimely death. At 35, after marriage and taking a home loan, she buys an additional Rs. 1 crore term life insurance policy to provide coverage for her spouse and loan obligations. Later at 42, she adds another Rs. 50 lakh term insurance cover for future education expenses of her 2 children. Currently, Anuradha holds three policies: Rs. 50 lakh + Rs. 1 crore + Rs. 50 lakh = Rs. 2 crore total cover amount.

If Anuradha passes away during the policy term, nominees of Anuradha’s term insurance covers can claim death benefits from all three plans mentioned above, provided full disclosures were made at the time of their purchase.

During purchase of a term life policy, your premium is usually determined after assessing your risk profile, which is calculated on the basis of your age, your current health status, medical conditions if any and lifestyle habits that are impacting your health. If you were a non-smoker and a non-drinker back then when you had originally bought the term insurance, your risk profile would have been estimated differently compared to what your current risk profile is after developing those habits.

Good news: Your premium does not automatically change immediately based on the lifestyle habits you adopt. Term life policy gives you enough predictability and long-term affordability by locking in the premium determined for you at the start of the tenure (provided you pay it regularly). In other words, your current policy with the insurer remains intact without any modifications even after you have developed these habits.

What’s ideally recommended?: You are expected to inform the insurer about significant and major developments to your health or anything to do with your changed lifestyle, either during periodic medical reviews (as and when required), policy renewal or while making a claim to the company. It is considered to be an important responsibility at your end because if something happens to you and your untimely death gets connected to your lifestyle changes (smoking, drinking etc.), your family’s claim for the payout can be denied or delayed depending on the case and the investigation findings. Therefore, honesty is always the best policy when it comes to term insurance. In case you were a smoker / drinker right from the start but had informed the insurance company otherwise (during purchase of the policy), this amounts to non-disclosure (hiding of such crucial information) which again leads to several complications during the claim, most of them putting your family’s peace of mind, protection, finances and future at a huge risk. This, in turn, destroys the whole purpose of why you had purchased a term life policy in the first place.

In short: Being transparent at all times ensures that your family doesn’t have to go through any such stress later. Upon intimation of your newly-developed habits and health changes, your insurer may reassess your risk profile. You can also expect your premium to increase accordingly.